A what?! You might ask...

Well this is the very reason why you need to read this blog post then!

Here is what you will learn today:

1. So what is my Fico score?

2. When do you need the best scores?

3. I checked my score and it's awful!?!

4. Know your FICO® scores, improve your FICO scores, save money!

1. So what is my Fico score?

Most people don't really care about the health of their credit score until the very last minute when their scores needs to shine bright and to score high!

In a nut shell you have 3 major scores bureaux:

Equifax

TransUnion

Experian

By law, each one of these bureau can provide you with a free copy of your credit report once a year. BUT this is only your report, you don't get the score and you have to pay for the score.

(if you just want the 25% off coupon on dont want to read the end of the blog, click here)

A lot of companies offeres you to check your score, and this is good BUT they don't offer the FICO score, just another type of score, often called a Power Score or they are using other names.

Fico score are the king of the hill when it comes to what the banks are looking for.

Credit score are vital to remain as high as possible and healthy, so you can get the best rate which in terms will save you money.

2. When do you need the best scores?

In everyday life actually!

For example in real estate: whether you are looking to buy a homes in Carlsbad near Oceanside and Encinitas, sell you condo in downtown San Diego Metro cities (if you are looking to buy another home) or refinance your Del mar beach front estate, or perhaps leasing that single family detached home in Rancho Santa Fe during the off season, all of these steps requires you to show off your credit score. Ask you local lender for details.

For example in car shopping: whether you are looking to buy a new car in Carlsbad at the Car Mall, dreaming to own one of those exotic and fancy car sold in La Jolla or in order to refinance your work truck all, of these steps requires you to show off your credit score.Ask you local car dealer for details.

For example while clothes or show shopping at the mall or online: whether you are looking to buy a new dress for your cocktail party in Rancho Santa Fe or a new hat for the Del Mar horse Races in one of those flag store, most of them will offer you some rewards for using their store credit card, etc...Ask you local store for details.

For example while hunting down a deal at your local hardware store: whether you are looking to buy some paint to get your nursery ready or your son is now off to college and you want to turn his bedroom into your ultimate at home office, most large store such as Lowes or the Home Depot of them will offer you some rewards for using their store credit card, even 6mo to 18mo with no interest on large purchases or large projects. I opened a project card several years ago and it turn out very handy anytime we need it. Ask you local store for details.

You even need it for opening a gas or electric bill, even a water bill in some states.

And don't forget in today's economy that you can even be turned down for a job based on your credit history so you get my point, check your credit (I have a free promo code below to offer you 25% OFF), cultivate your credit and pull those bad weeds out and watch it bloom for a healthy score and in turn, lesser money out of your pocket and more in your bank for you to keep!

3. I checked my score and it's awful!?!

Ok this stinks, but this is not the end of the world, you're score constantly flactuate and can improve.

Check some tips here to pump up your Fico score to new hights: Fico tips.

4. Know your FICO® scores, improve your FICO scores, save money!

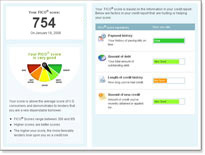

Click to see larger image

Click to see larger imageWhether you’re buying a home, a car or applying for a credit card – lenders want to know the risk they’re taking by lending your money. FICO scores are the credit scores that most lenders use to determine your credit risk. Your FICO credit scores (you have 1 score from each of the 3 major credit bureaus) can affect how much money a lender will lend you and at what terms (interest rate). So, taking steps to improve your FICO scores can often help you qualify for better rates from lenders – which can save you money!

Take a look at the example FICO score report and you can see that it shows your FICO score in big bold numbers as well as a general indication of how your score relates to other U.S. consumers (bad to great). FICO scores range from 300-850 – higher is better. You can also see that your FICO score looks at several major categories as shown by the key ingredients on the right side of the sample report. For more information about these general categories, see the What's in your score page.

Your FICO score is calculated using the information in your credit reports. These reports contain all of the information that each credit bureau has on file about you. This sample credit report shows a few examples of the types of information that the credit bureaus collect, such as your credit accounts, how many times lenders have requested information about your credit (Inquiries), and how many times lenders have turned your account over to a collection agency (Collections).

0 comments:

Post a Comment